Education

To create profitable and innovative partnerships through real estate investing with the purpose of enhancing the lives of our partners and colleagues, while strengthening local communities.

-

ARTICLE

1031 EXCHANGE

What Is a 1031 Exchange and Why Is It Important?

If an individual exchanges one investment property for another via a 1031 exchange, they may be able to defer capital gains or losses that they would otherwise have to pay at the time of sale.

Read More...

What Is a 1031 Exchange and Why Is It Important?

A “1031 exchange” is the nickname used to discuss Section 1031 of the U.S. Internal Revenue Service’s tax code. This section states that if an individual exchanges one investment property for another via a 1031 exchange, they may be able to defer capital gains (or losses) that they would otherwise have to pay at time of sale.

Section 1031 applies to “property” beyond real estate, but many 1031 cases deal with buildings and land. We’ll only discuss 1031s in relation to real estate.

WHY IS A 1031 EXCHANGE IMPORTANT?

So why is a 1031 exchange important? It allows real estate investors to defer paying capital gains and potentially build wealth through real estate investing.

Think about it this way. If you buy a piece of real estate for $100,000 and then sell it for $500,000, you are subject to paying capital gains taxes on your $400,000 profit. From that $400,000, you would lose, say, $120,000 to capital gains taxes. With a 1031 exchange, you might be able to use the $500,000 to purchase one or more new properties and pay no capital gains taxes at the time of sale. The sale’s proceeds fund new investment properties, which in turn may generate cash flow and appreciate.

While you’ll eventually have to pay taxes when you sell these new properties, you may be able to make your money go further using a 1031 exchange. These exchanges matter because they can help real estate investors create more wealth. Investors may use 1031 exchanges throughout their careers to buy bigger or better properties and potentially reap the rewards.

TYPES OF PROPERTIES THAT QUALIFY

What types of properties quality for a 1031 exchange? The short answer: it depends. That’s because the language used in the tax code is vague. Properties must be, it says, “like-kind.” Says the IRS

“Both properties must be similar enough to qualify as ‘like-kind.’ Like-kind property is property of the same nature, character or class. Quality or grade does not matter. Most real estate will be like-kind to other real estate. For example, real property that is improved with a residential rental house is like-kind to vacant land. One exception for real estate is that property within the United States is not like-kind to property outside of the United States. Also, improvements that are conveyed without land are not of like kind to land.”

Are you confused about exactly what “like-kind” means? You’re not alone. Says tax expert Robert Wood

“Most exchanges must merely be of ‘like-kind’–an enigmatic phrase that doesn’t mean what you think it means. You can exchange an apartment building for raw land, or a ranch for a strip mall. The rules are surprisingly liberal. You can even exchange one business for another. But again, there are traps for the unwary.”

This is why it is essential to secure professional help if you’re considering a 1031 exchange—there are pitfalls aplenty even for seasoned investors.

RESTRICTIONS ON 1031 EXCHANGES

Investors must consider additional restrictions, beyond the definition of “like-kind.” A tax professional will illustrate each one, but a few major considerations include:

You must own the real estate. Owning a share in a REIT, a fund or an LLC that owns a share in another LLC does not qualify.

You can only perform a 1031 exchange between investment properties. You can’t do this with personal property.

If you exchange for a cheaper property, you’ll face tax considerations around the price difference.

You can “delay” your exchange (which most people do), where a third party acts as an intermediary between you and a prospective future buyer.

While you can delay the exchange, there are important timing restrictions on the deal. Says the IRS:

“The first limit is that you have 45 days from the date you sell the relinquished property to identify potential replacement properties. The identification must be in writing, signed by you and delivered to a person involved in the exchange like the seller of the replacement property or the qualified intermediary. However, notice to your attorney, real estate agent, accountant or similar persons acting as your agent is not sufficient."

There’s a second deadline, too. The “property must be received and the exchange completed no later than 180 days after the sale of the exchanged property.”

As you can see, 1031 exchanges offer immense benefits. But their execution is tricky. Plenty of caveats wait to ensnare investors. If you don’t get the whole deal right, you may end up paying taxes on the entire sale.

-

ARTICLE

ALL ABOUT REITS

5 Important Things To Consider Before Investing In A Multifamily Property

In this article, we discuss some of the due diligence that is routinely undertaken by our management team in evaluating apartment buildings for potential addition to our multifamily REIT.

Read More...

5 Important Things To Consider Before Investing In A Multifamily Property

At Ram Realty Trust, we offer all members access to the multifamily sector of commercial real estate through investment in our private, non-traded REIT, RAM REIT I.

In this article, we discuss some of the due diligence that is routinely undertaken by our management team in evaluating apartment buildings for potential addition to our multifamily REIT.

To begin - as a general rule, the value of any income property is a function of the cash flow it generates. Sometimes investors are willing to pay very high prices (low capitalization rates) because they expect significant ongoing increases in the cash flow of a property, or because the value of the land offers a separate source of value. This is not usually true of apartment buildings; cash flow typically grows over time, but physical and functional obsolescence, and sometimes local rent control, usually cause cash flow growth expectations to remain modest.

1. LOCATION

The area or community in which an apartment complex is located is of prime importance. The regional economic drivers and employment levels are important, but a more detailed study of the particular neighborhood of the property is also essential. Is the area already popular, or at least seeing an upswing in perceived appeal?Are other neighborhood demographics, like the age distribution and average household size, favorable to apartments? Local economic activity is also important. Are new jobs likely to be created nearby, or are nearby base industries on the decline? Access to transportation is also valuable – are freeways or light-rail lines nearby to provide access to downtown areas or other employment centers?

2. PHYSICAL PLANT

As with any property, the physical state must be assessed to evaluate deferred maintenance items that can materially affect the operation and value of the apartment building. A prospective owner should evaluate the plant’s foundation, roof, heating and air conditioning systems, electrical, plumbing, elevators, and the building’s “envelope” (the windows and walls). Expected future repairs or improvements should be analyzed with an anticipated timeline and the associated costs, in order both to better negotiate the purchase price of the property and to perform appropriate financial planning for the investment.

3. COMPETING SUPPLY

Construction cycles occasionally result in an over-supply of apartment buildings and other commercial properties. An analysis of new construction permits and other housing statistics can provide a feel for whether the property is in a relatively stable market or one where competing properties are shortly due to come on-line. Construction is also affected by local or regional restrictions such as zoning, building codes, and environmental impact studies and fees. Over the long run, such restrictions may cause local price appreciation to be greater than in other areas.

4. VACANCY RATES

Complexes with more than 7-8% vacancy rates tend to be either in an unfavorable market area or in need of renovation or other re-positioning. Sometimes, however, such adverse figures are simply due to poor management. Apartment buildings are management-intensive, and tenant relations, proper maintenance, and the showing and renting of space are key components of the property manager’s responsibilities. A review of current and historical occupancy rates, both for the property and for comparable properties in the area, can give an investor a better understanding of a property’s potential competitiveness.

5. VALUE-ADD OPPORTUNITIES

Sometimes a smartly chosen remodeling project can markedly boost the attractiveness (and rental rates) of a property. A re-fashioned façade, or the remodeling of kitchens and baths as units become vacant, can oftentimes justify higher rental rates and increased cash flow. Apartment buildings are also often in a position to generate ancillary sources of income. Coin-operated laundry facilities (using energy-efficient equipment) and vending machines are some of the best sources. Parking spaces can often be charged for separately, and are usually not subject to rent control regulations. Mini-warehouse facilities and furniture rental arrangements, among other things, can also add to a property’s top line.

A key aspect of any passive investment is to also perform due diligence on a project’s sponsor. Operators with a track record and a solid understanding of the local market are often well positioned to update poorly performing properties and run them more efficiently.

Interested in learning more about multifamily investing or RAM REIT I?

Visit the investment opportunity page here, or email our Investor Relations team today.

-

ARTICLE

ALL ABOUT REITS

Traded vs. Non-Traded REITS

There are different types of REITs you may invest in. The guide below is intended to give you some of the information you need to decide which type of REIT is best for you.

Read More...

Traded vs. Non-Traded REITS

Once you have made the decision to invest in real estate, you will want to identify specific opportunities that meet your investment goals. You have put in the time and have done your research and know that due to the instant diversification and stream of income from paying out almost all their profits each year, a Real Estate Investment Trust or “REIT” may be the right investment for you.

Just when you thought all your decisions were made, you find out that there are different types of REITs you may invest in. Ultimately, the decision comes down to your individual main goals and objectives. The guide below is intended to give you some of the information you need to decide which type of REIT is best for you.

MAIN TYPES OF REITS

REITs can be public or private, traded, or non-traded. The three main types of REITs are 1) private REITs, 2) public non-traded REITs, and 3) publicly traded REITs. Each type has distinct characteristics and its own set of advantages and disadvantages.

1. PRIVATE REITS

Not SEC Registered: Private REITs are not registered with the Securities and Exchange Commission (the “SEC”) and not regulated by the SEC.

Not Listed: Shares of private REITs are not listed on a public exchange such as the New York Stock Exchange (“NYSE”). This means their shares are not directly affected by stock market volatility.

Performance Information: Typically, there is little to no public information released about private REITs so it is often difficult to obtain performance information unless you are invested in the private REIT.

Who can Invest: Private REITs are available for investment only by accredited investors, which on a high-level are individuals who have either over $1 million in net worth, excluding their personal residence or have made at least $200,000 a year for the past two years. As they are not regulated, the SEC wants to ensure that only experienced investors that have disposable income are investing in these types of vehicles.

Investment Minimum: Private REITs offered to retail investors often have a minimum investment amount of anywhere between $10,000 to $100,0000, and the upfront costs for Private REITs vary by company.

Liquidity: If you want to pull out your funds before a liquidation event, it might be difficult as redemption programs vary by company and are often limited.

2. PUBLIC, NON-TRADED REITS

SEC Registered: Public, non-traded REITs are required to file with the SEC and are therefore regulated.

Not Listed: Shares of public, non-traded REITs are not traded on a national stock exchange such as the NYSE. Which, much like private REITs, means their shares are not directly subject to stock market volatility. These types of REITs do not deal with daily price changes like publicly traded REITs, which allow the managers to focus on long term objectives instead of focusing on daily price changes and quarterly earnings.

Performance Information: Though these REITs are not traded on an exchange, because they are registered with the SEC, there are required SEC filings and performance reporting is publicly available. In general, due to the long-term nature of the real estate market and the work involved in closing each transaction, the objective of many real estate managers and investors is to hold on to real estate investments for the long term.

Who can Invest: Public non-traded REITs are available for investment by anyone, whether accredited or non-accredited, subject to certain investment limits.

Investment Minimum: The minimum investment for a public non-traded REIT typically starts around $1,000 but may vary. Many non-traded REITs charge high upfront fees that may be as much as 15% of the per share price according to FINRA. However, in the past few years, technology savvy non-traded REITS are working to redefine the industry by charging lower upfront fees. Our REIT, RAM REIT I charge 0% as an upfront fee to our investors.

Liquidity: Like private REITs, because the shares of non-traded REITs are not traded on an exchange, redemption programs are often limited and vary by company.

3. PUBLIC, TRADED REITS

SEC Registered: Public traded REITS are registered with the SEC and regulated.

Listed: In contrast to both private REITs and public non-traded REITs, publicly traded REITs are listed on a stock exchange and as such are subject to the volatility of the stock market.

Performance Information: As they are registered and regulated, a wide range of public information is available both by the company that owns and manages the REIT, and independent sources. As publicly traded REITs are liquid, visible to the public, and have daily pricing changes, there may be pressure to focus on short-term quarterly earnings instead of long-term investment objectives. It may also be hard to raise capital when the market is down.

Who can Invest: Anyone may invest in publicly traded REITs with a minimum investment of one share (at the current share price). The upfront fees are charged by the broker that you purchase your shares though and may be the same as you would pay for buying or selling any other publicly traded stock.

Investment Minimum: The minimum investment for a public non-traded REIT may vary, however they typically start at around $1,000 to $2,500.

Liquidity: Unlike private REITs and public non-traded REITs, publicly traded REITs are liquid and may be traded every business day, which means they are easy to redeem.

SUMMARY

Overall, which vehicle you choose to make your REIT investment in real estate is dependent upon what your current goals and objectives are, among other variables. Some of the questions you should ask yourself before choosing what type of REIT investment to make are: What is important to me? Am I looking for a more liquid investment like a publicly traded REIT?

If so, are you comfortable with daily price fluctuation and market volatility exposure? Or is your goal to invest real estate as directly as possible? While non-traded REITs were often shunned due to their high fees, many companies, including Ram Realty Trust, have made it possible to charge the investors lower up-front fees and put more of your money to work for you.

LEARN MORE ABOUT RAM REALTY TRUST’S REITS:

RAM REIT I invests in a variety of commercial properties via debt and debt-like securities. The primary objectives of RAM REIT I are to pay attractive and consistent cash distributions, and to preserve, protect and increase an investor’s capital contribution.

For more information, please review the Disclosure Document prior to investing.

Investing in the Company’s common shares is speculative, involves substantial risks, and is not suitable for all investors. Before investing, consider the “Risk Factors” section outlined in the offering circular detailing risks, including, but not limited to, illiquidity, complete loss of capital, limited operating history, conflicts of interest and blind pool risk. Past performance is not indicative of future results. Investment information contained herein has been secured from sources Ram Realty Trust believes are reliable, but we make no representations or warranties as to the accuracy of such information and accept no liability. We suggest that you consult with a financial advisor, attorney, accountant, and any other professional that can help you to understand and assess the risks associated with any investment opportunity. -

ARTICLE

BUILDING WEALTH

Retirement Investing in Real Estate: New Opportunities

Learn how to invest your retirement account in real estate stocks, mutual funds, publicly traded REITs, or directly in real estate.

Read More...

Retirement Investing in Real Estate: New Opportunities

Retirement investing today offers a great deal more freedom and choices for investors than it ever has. Whereas historically most individuals invested their IRAs, 401(k)s and other qualified retirement accounts in traditional vehicles such as stocks, bonds, mutual funds and Treasury notes, today investors can use their retirement accounts to invest in a number of other types of assets.

In this article you will learn:

How to invest your retirement account in real estate stocks, mutual funds, or publicly traded REITs

How to invest your retirement account directly in real estate

How to borrow against your 401(k) or IRA to invest in real estate

How to invest your 401(k) or IRA through a crowdfunding platform

How to invest your self-directed IRA in a non-public REIT

One of the most popular non-traditional asset classes for retirement investing is real estate. Many investors view real estate’s potential for long-term appreciation, combined with the tax advantages of a qualified retirement plan, as potential reasons to invest their retirement accounts in real estate.

This page will discuss several of the ways individual investors can use their personal retirement accounts to invest in real estate, as well as the potential benefits and risks involved.

HOW CAN I USE MY RETIREMENT ACCOUNT TO INVEST IN REAL ESTATE?

Retirement investing in real estate is a broad concept that can involve many types of investment vehicles, varying amounts of risk, and different degrees of involvement required on the part of the investor. Here are a few examples.

1. You can invest your retirement account in real estate stocks, mutual funds or publicly traded REITs (real estate investment trusts)

This is the most common way of using a personal retirement account to invest in real estate.

If you own an IRA, you can simply use your account to purchase equity shares (or debt shares, by buying bonds) of real estate-related businesses. These could be publicly traded real estate development companies or mortgage companies, for example, or mutual funds or publicly traded REITs (real estate investment trusts) that are themselves invested in a basket of real estate businesses.

If you have a 401(k) through an employer, you might also be able to find real estate-related investment opportunities such as these in your plan’s available offerings. Generally speaking, however, an employer-sponsored 401(k) can have a more limited range of investment opportunities for you to choose from than your personal IRA might have.

With that in mind, if you have a 401(k) with your employer and cannot find the right real estate-related investments for your retirement account, you can also open an IRA — either a traditional IRA or a Roth IRA — and find real estate investments through that account. But you will need to do your due diligence first, because there are limits on an IRA that you hold if you also maintain a 401(k), and you will want to learn about the tax implications of owning both retirement accounts simultaneously as well.

This is the most passive and straightforward way to invest your retirement account in real estate. In essence, you can simply find stocks, bonds or mutual funds to purchase, just as you would with other types of traditional retirement investing. The only difference, in this case, would be that you have chosen real estate as the industry in which to invest.

2. You can (in some cases) invest your retirement account directly in a piece of real estate

This is a far more active — and risky — means of using your retirement account to invest in real estate. But if you know what you are doing, and you’ve thoroughly researched the laws, restrictions and tax implications, it is also a potentially lucrative way to grow your retirement nest egg.

First, it is important to understand that although investing IRA funds directly in a piece of property is entirely legal, many IRA administrators will not allow such investments. If you’ve opened an IRA with a financial-services company that does not allow direct real estate investing, you might want to find a new plan — typically called a self-directed IRA — that allows such investments.

Another option for you might be a Solo 401(k) — a personal retirement account for individuals with single-person businesses or consulting practices and with no employees. If this describes you, you might also consider opening a Solo 401(k), which can allow you to use your account to purchase real property directly.

Next, you’ll need to know the limitations of direct real estate investments through your IRA or Solo 401(k). For example, the IRS’s Prohibited Transactions Rules prevent what the tax agency calls “self-dealing.” This means if you purchase a home or office through your plan and then rent it out to a family member, employee or yourself, you might be hit with taxes or other penalties. When you purchase property through one of these qualified retirement plans, then, you need to be sure that neither you nor those close to you are ever involved on the other side of the deal. In other words, you will want to keep all transactions relating to this real estate — who’s occupying the property, who’s paying the rent, who’s guaranteeing the mortgage, etc. — at arm’s length, meaning not involving people in your immediate social or professional circles.

There are also other potential pitfalls that can ensnare an investor who purchases real estate through an IRA or Solo 401(k). For example, if the property must be sold during a time in which the real estate market is down — because, for example, you have reached the age of your plan’s required minimum distribution (RMD) — you might have to sell the property for less than you had hoped for.

Another key issue here is that, when you purchase a property through a retirement account, all of the business income, such as rent, that the property earns will need to be deposited directly back into the retirement account itself. If you take any of that income out and put it in your own bank account, it will be subject to taxation and possibly some hefty penalties as well.

For these reasons, although investing your IRA or Solo 401(k) directly in a piece of real estate has historically had potential for returns over time, you will need to thoroughly research this type of investment and learn about the restrictions, tax issues, and risks before making such a move.

3. You can (in some cases) borrow against your IRA or 401(k) to invest directly in a piece of real estate

Some retirement plans, including Solo 401(k)s and some of the standard, employer-sponsored 401(k) plans, allow account holders to borrow money from their retirement accounts and then use these funds to purchase real estate.

Keep in mind that in such a case the real estate itself is not held inside the retirement account — which means it won’t be enjoying the tax-deferred earnings benefits that the plan provides. The potential benefit here would simply be that the investor could tap the funds in the account and — provided she pays the loan back according to the plan’s schedule — enjoy access to that investment money without tax or penalty.

There is, of course, substantial risk here as well. Owning an individual piece of real estate requires active attention to the property and carries the risk of loss — loss of tenants, property damage, loss of equity in a down market, etc.

Moreover, if you were to use your employer’s 401(k) plan to borrow the money to purchase a piece of property, you could face an additional risk — a significant one. Assuming you took out a mortgage to buy the property, if you lost your job, your entire outstanding mortgage balance might come due immediately.

For these reasons, you will need to conduct thorough research and educate yourself on all of the tax implications, legal ramifications, and financial risks before borrowing against your retirement account to fund a real estate investment.

4. You can (in some cases) invest your IRA or 401(k) directly in real estate deals through a real estate crowdfunding platform

This is among the newest and most innovative ways to invest directly in real estate using your retirement account. And in a sense, it has the potential to provide you with aspects of both passive and active real estate investing.

When you invest in real estate through a mature, established real estate crowdfunding platform, such as Ram Realty Trust, you have the opportunity to participate in commercial real estate deals previously available only to large investment houses and wealthy individuals.

With the right crowdfunding platform, for example, you can make equity or debt investments directly in specific commercial properties — thoroughly vetted by a team of real estate and finance experts — and participate in the possible upside of those deals. These might be industrial or retail properties, or large apartment or condominium complexes. You can also search for the most attractive individual deals for you by geographical region or even by stage of completion. In other words, rather than investing in a publicly traded real estate mutual fund — itself spread across hundreds or thousands of real estate businesses — you can invest directly in a single, large-scale commercial real estate deal.

At the same time, you will be able to make this direct investment in property without any of the active, hands-on work required for traditional real estate ownership. You won’t be responsible for the tenants, the upkeep or maintaining the books — that will all be managed by the owners and experts.

In other words, this can be simultaneously a direct, passive investment in commercial real estate. As with all types of investment you will need to thoroughly research this type of investment and learn about the restrictions, tax issues, and risks before making such an investment.

Learn how to leverage your retirement account to invest in commercial real estate deals through our crowdfunding platform, either by opening a new Ram Realty Trust IRA or funding an existing IRA or 401(k).

5. You can even invest your self-directed IRA in a non-public REIT

This new form of retirement investing in real estate is another way that you as an individual investor can gain access to a non-public real estate opportunity that you might not otherwise be able to.

In 2021, Ram Realty Trust began accepting retirement funds from self-directed IRAs into the company’s online, income-producing REIT, called RAM REIT I.

With as little as a $1,000 investment through your qualified IRA, you can now invest in commercial real estate and enjoy the potential for both passive incomes accumulating in your retirement account. You can also automatically reinvest your dividends back into RAM REIT I, thereby offering the possibility of compounded returns over time.

Additionally, Ram Realty Trust can also accept rollover funds from your existing retirement plan and serve as the custodian of record for your new IRA, to be invested in RAM REIT I. This service will be free of fees for the first year and will require only a $10,000 minimum investment. Keep in mind there are risks to investing in the RAM REIT I so it is important to review the full offering materials.

For more information, please review the Disclosure Document prior to investing.

-

ARTICLE

BUILDING WEALTH

How to Harness the Power of Your Real Estate Portfolio

Forbes calls real estate “the third-largest source of wealth among the ultra-rich”. How do you potentially optimize the return on your property investment and harness the power of your real estate portfolio?

Read More...

How to Harness the Power of Your Real Estate Portfolio

Having a real estate portfolio may make you feel like a smart investor. After all, real estate has long been a fairly reliable way to build wealth—Forbes calls it “the third-largest source of wealth among the ultra rich—and numerous tax advantages only sweeten the deal. But even owning lots of property doesn’t guarantee a high-performing portfolio, or one that’s immune to changing market conditions.

So, how do you potentially optimize the return on your property investments—and harness the power of your real estate portfolio?

DIVERSITY IS KEY

When conditions change, so does demand for different types of real estate. Accordingly, it makes sense to mix up your portfolio by including property of different types, located in different areas and valued at different price points. Holding look-alike properties can hold your portfolio back—and undermine the “get rich through real estate” dream.

Investing in the aforementioned property mix, while having your ear to the ground so you know which markets are growing (most likely to perform well) and which have matured (the thrill is gone), can be a great portfolio diversification recipe. Oh and don’t forget about having good management in place to keep things running smoothly on the ground. While this may be challenging, somewhat stressful and time-consuming, it is totally doable, right?

Or, you can trust the experts to do all the above for you.

One way to reap the potential rewards and minimize the challenges of property ownership is through passive real estate investing. Why not let the pros do all the heavy lifting when it comes to vetting properties, along with all the financing, managing and even reporting aspects of owning numerous properties? This will free your time to enjoy the benefits of being a commercial real estate owner.

Through passive real estate investing tools like crowdfunding, you can tap the “power of the crowd,” like-minded investors who share the returns and the risk. And you can benefit from the expertise of real estate, finance and technology gurus—like those behind an industry leader like RamRealtyTrust.com—while gaining access to a powerful real estate diversification tool: real estate investment trusts. Known as REITs, these funds not only enable you to invest in commercial real estate, but to own a variety of it—bringing diversity to your portfolio and providing you income streams in the form of rental payments.

INVESTING IN COMMERCIAL REAL ESTATE CAN BE A GREAT WAY TO DIVERSIFY

Investing in different types of commercial real estate properties, each with different economic drivers, is the perfect way to avoid holding look-alike properties that can make your real estate portfolio vulnerable. In general, commercial properties include:

Office property – Can be classified as Class A, B or C, depending on construction quality and location (A being best of both worlds), Central Business District (or “CBD,” such as downtown high rises in medium and larger cities) and suburban office buildings (campus-like office parks in the ‘burbs).

Industrial property – Includes heavy manufacturing, light assembly, flex warehouse (a mix of industrial and office space) and bulk warehouse (e.g., distribution centers).

Retail property – Can consist of small (strip) to large (“power”) shopping centers, regional malls and out parcels, which are parcels of land within a center that are leased to individual tenants, like banks or fast-food places.

Multifamily – Properties like suburban garden apartments, urban midrise apartments and professionally-managed high-rise apartments that are found in larger markets.

Self-Storage – A property with storage units or spaces that are rented to tenants, often on a monthly basis.

Recently, RamRealtyTrust.com announced the launch of RAM REIT I, its first crowdfunded REIT. Designed to offer investors single investment access to a diversified pool of commercial real estate with minimum investments as low as $1,000, RAM REIT I seeks to democratize real estate investing. And because of the exclusive and direct access it gives investors to the product, the fund can do so at a low cost—investors pay no sales commission and other upfront costs are estimated at only 0%.

Says RamRealtyTrust.com CEO Ram Kalagara, “Beyond the zero commissions and lower fees, the fund’s strategy is exciting because it allows us to leverage RamRealtyTrust.com’s hundreds of inbound inquiries for financing on commercial real estate and curate them to find suitable opportunities.” Keep in mind that real estate investing has risks, including risk of loss, and is not suitable for all investors.

With RAM REIT I, the timing is even better to consider “joining the crowd” at RamRealtyTrust.com and diversifying your portfolio through REIT investment. For more information on RAM REIT I, contact us today and review the Disclosure Document.

-

ARTICLE

COMMERCIAL REAL ESTATE

6 Common Real Estate Crowdfunding Myths Debunked

As featured on Inman.com. Here we describe the 6 common real estate myths and why they cannot be true.

Read More...

6 Common Real Estate Crowdfunding Myths Debunked

As featured on Inman.com

KEY TAKEAWAYS

It’s often the size of the deal, not quality, that drives a sponsor’s decision to crowdfund.

High deal volume is not necessarily an indicator of success.

As with any product or service, some crowdfunding platforms are better than others.

Crowdfunding — using an online platform to “pool money from the crowd” to facilitate funding of new investment opportunities — has been a hot idea for years. Thanks to changes in regulation, developments in technology and the internet’s ability to connect people and information quickly and effectively, small businesses have the potential to raise capital like never before.

Likewise, investors can participate in previously inaccessible opportunities from their laptop or tablet, which makes the whole process fast, convenient and efficient.

By bringing together real estate companies with individual investors, real estate crowdfunding has certainly helped disrupt the way people find and invest in properties. According to Crowdsourcing.org, real estate crowdfunding is projected to reach $3.5 billion in 2016. As the industry evolves, all signs indicate real estate crowdfunding is here to stay and will continue to grow.

"Real estate crowdfunding is projected to reach $3.5 billion in 2016."

There are some real estate entrepreneurs and investors, however, who haven’t yet embraced these online platforms. For those who hesitate to join the crowd, here are six common crowdfunding myths and the truths that bust them:

MYTH 1: ONLY BAD DEALS END UP ON CROWDFUNDING WEBSITES BECAUSE THEIR SPONSORS CAN’T GET CAPITAL ANYWHERE ELSE.

Truth: Choosing to crowdfund has nothing to do with deal quality.

Often, it’s the size of the deal, not quality, that drives a sponsor’s decision to crowdfund. The small balance commercial market — say, loans or equity contributions that fall in the $1 million to $5 million range — have been largely underserved since the financial crisis, thanks to increasing bank regulatory costs.

Additionally, with crowdfunding, borrowers and sponsors skip the hassle of managing multiple investor relationships, distributions and tax reporting because online platforms do that for them. So, choosing to crowdfund can also be about convenience.

Finally, through crowdfunding, real estate companies get incredible access to a much larger network of investors, which makes it easier to raise capital as needed. So, a desire for access to more investors might also drive a decision to crowdfund.

Real estate investments carry risks, do not guarantee a return of any kind and can include the loss of your entire investment. But rest assured, a reputable platform will do its due diligence and thoroughly screen deals before placing them on the marketplace for investors to fund.

The platform’s very reputation and survival depends on it.

"Often it's the size of the deal, not quality, that drives a sponsor's decision to crowdfund."

MYTH 2: CROWDFUNDING PLATFORMS ARE JUST MARKETING WEBSITES THAT PRESENT A THIRD-PARTY PRODUCT WITH NO DILIGENCE. ESSENTIALLY, CROWDFUNDING IS ‘EBAY FOR REAL ESTATE.’

Truth: As with any product or service, some crowdfunding platforms are better than others.

Yes, as mentioned above, there are crowdfunding platforms that don’t do their due diligence. Others are meticulous about vetting deals and even fully underwrite every one they offer.

With real estate intermediaries, it’s important to have complete transparency. Are proformas available? Third-party reports? Market data? Track records of the sponsor so that you can review previous performance?

Good platforms make all these and more available to investors, so you can choose deals that align with your investment goals.

MYTH 3: ALL CROWDFUNDING PLATFORMS ARE THE SAME.

Truth: Not even close. The product and the people behind a platform are everything.

Crowdfunding platforms can vary extensively, depending on the product and the team behind it. When choosing a platform, it’s important to recognize that the product is affected by the level of deal screening and the types of investment being offered.

For example, does the platform focus on deals offering cash flow, or does it concentrate on appreciation through land development? Does it fully underwrite each transaction on its platform? Does it perform site visits or trust third-parties only?

Some platforms boast a team of professionals who are best in the field of real estate, finance and technology; others are staffed by people who are less experienced and less credentialed.

When choosing a crowdfunding platform, put your trust where the product you want meets the team with the most collective knowledge, experience and integrity.

MYTH 4: PLATFORMS WITH MORE DEALS ARE BETTER.

Truth: High deal volume is not necessarily an indicator of success.

Just because a platform offers more deals doesn’t mean those deals are good. Having high volume could mean the company does less screening and simply originates a lot of deals to boost numbers — a quantity-over-quality approach that doesn’t prioritize investor protection.

To identify better platforms, instead look for a stated commitment to vetting and underwriting deals, being transparent with information and otherwise protecting investors against risk.

"High deal volume is not necessarily an indicator of a crowdsourcing platform's success."

MYTH 5: IF A CROWDFUNDING PLATFORM GOES OUT OF BUSINESS, I’LL LOSE ALL MY MONEY.

Truth: Good platforms structure transactions in a way that protects investors in such event.

There’s cause for concern if a crowdfunding platform shuts its virtual doors — and a good deal of comfort to be had from a platform that is well-funded.

How do you mitigate any potential bankruptcy-related loss? By choosing a platform that structures its deals in a way that protects investors and that has a bankruptcy contingency plan in place.

Does the platform use Special Purpose Entities (SPEs), which create bankruptcy remoteness? Is there a reputable third party that will step in if the platform’s viability is at risk? Research these things before investing to minimize or even prevent your loss in the event of a platform’s demise; because remember, there are no guarantees when it comes to investing.

MYTH 6: AS AN INVESTOR, I’M BETTER OFF WORKING DIRECTLY WITH THE SPONSOR.

Truth: Not necessarily. There are some advantages to investing indirectly.

First, as an investor, you get access to more sponsors and more deals if you join an online platform.

Secondly, the “power of the crowd,” by definition, can bring with it “the benefits of the many” — like specific voting and decision rights that might be unavailable if you invest as an individual on your own.

Finally, the expertise the platform provides, through its team of behind-the-scenes professionals, helps protect investors and ensure they have a consistently good user experience across all investments, regardless of origin.

At the end of the day, real estate crowdfunding seems more and more like the wave of the future — and the great evolving ride of the present.

Although to some it might still be the new kid on the block who comes with all sorts of risk and mystery, a bit of knowledge can help you recognize the better platforms out there — and start benefiting from this potentially profitable and growing trend in real estate financing and investment.

-

ARTICLE

COMMERCIAL REAL ESTATE

Commercial Real Estate Waterfall Models for Private Placement Offerings

A waterfall, also known as a waterfall model or structure, is a legal term used in an Operating Agreement that describes how money is paid, when it is paid, and to whom it is paid in commercial real estate equity investments.

Read More...

A waterfall, also known as a waterfall model or structure, is a legal term used in an Operating Agreement that describes how money is paid, when it is paid, and to whom it is paid in commercial real estate equity investments. Distributions from cash flow and distributions from a capital event (i.e. a refinance or sale) of the investment property are allocated to the General Partners (GPs) and Limited Partners (LPs), primarily based upon the roles they play in a real estate transaction. These distributions are important because the waterfall may be determined based upon different methodologies that impact the net returns to investors, and the terms offered may change for different investments.

The General Partner’s Role

The General Partner is also called the “sponsor” or the “manager” or the “operating partner” because it generally has control over most decisions, including major ones like how much to spend on improvements, what rents to charge, and when to refinance or sell the property. Investors should be aware that many GPs expect to receive a promote, or outsized profit share, also sometimes called a carried interest. The promote is specific to their role in finding the transaction, negotiating the offer terms with the seller, performing due diligence, securing and signing onto the debt, and managing all aspects of ownership including any proposed renovations until disposition. The promote is meant to reflect the additional amount of time, effort, cost and risk that a GP takes on, while the potential return offered to passive LP investors does not. By giving LP investors a priority of cash flows, the GP is taking on more risk and aligning its upside with the eventual success of the project, since the GP has a more direct ability to impact that outcome than an LP.

Understanding IRR (Internal Rate of Return)

When first analyzing commercial real estate investment opportunities, it is important to determine whether the target internal rate of return (IRR) proposed is the deal level IRR or the net to LP investors level IRR.

The deal level IRR is the return based upon the inflows and outflows at the property level. While the deal level IRR may look good to an investor, it does not reflect the actual return that the investor receives or is expected to receive because it does not reflect the fees and the waterfall.

Rather, the return net to the LP investors is very important, as it reflects the actual projected inflows and outflows that the LP investors are underwritten to potentially receive, including the promote that the GP is proposing to take.

Working with a Real Estate Crowdfunding Platform

One of the benefits of working with certain crowdfunding companies such as Ram Realty Trust is that by aggregating smaller investors into a single purpose entity (usually a limited liability company, or “LLC”¹) the group as a whole is providing more capital than any individual investor. Although there may be fees required to account for the costs of putting the investment group together, the group is afforded greater voting rights and a greater ability to negotiate more favorable waterfall terms.

Breaking down a Waterfall Model

An example of a simple waterfall model may be a sponsor who offers an 8% preferred return and then a 70%/30% split. The sponsor here is telling investors that they should expect to receive their pro rata share of the distributable cash flow from a transaction until they have received an 8% return on their investment. Then all distributions will be paid to equity holders until initial investments have been fully returned. After that, the LP will receive 70% of the distributions, with the remaining 30% distributed to the sponsor as a “promote.”

From here there are a few questions that may arise:

If the 8% isn’t reached in a particular year, does it carry over (accrue) to the next year or does the preferred return reset each year into the project? This would be determined by the legal language in the operating agreement.

Is the preferred return compounded? When a preferred return is carried over to the following year (accrues), it is either compounding or non-compounding. For a compounding return, the preferred return rate (e.g. 8%) is applied to the accrued interest. So, if $10,000 carried over, $10,800 would be owed the following year.

Does the sponsor get the preferred return and Limited Partner returns on their capital invested? Often yes, the sponsor’s capital is treated pari-passu (meaning, on the same terms) as other capital unless negotiated otherwise.

Are all Waterfall models the same? No, each sponsor offers their own structure and it may be negotiated by investors with sufficient negotiating power (i.e., capital) to make sure the offered terms are reasonable compared to other like investments in the market and the belief that the project could reasonably reach a return that the investor deems is a good risk-adjusted return relative to other like projects in the market.

What happens if the preferred return is not reached? Investors take on the risk that a project may not reach the preferred return offered by the Sponsor, but if that occurs the Sponsor will also not achieve its promote. The purpose of the preferred return is to put the investor first for distributions since it is the investor’s capital at risk.

Do all transactions offer a preferred return? No, some projects do not offer a preferred return. There are several ways to structure a waterfall, which are described below.

The following describes the most common types of waterfalls available to investors:

1. IRR Lookback or “XIRR method”

The first method of determining the waterfall model for a project is the Internal Rate of Return (IRR) lookback or XIRR method. The IRR is a time value calculation of all inflows and outflows of capital, from the outflow of the investment at the time the transaction closes, to inflows of cash from the operations of the property during the hold period, and finally, the inflow of capital to investors upon sale of the property, hopefully with a profit. “XIRR” is the function used in Microsoft Excel that allows for distributions at different time periods. A positive IRR cannot be calculated until initial capital invested is returned to investors, so this methodology contemplates a full return of the investor’s initial investment, or principal, before the sponsor gets paid any promote.

For this methodology, a series of target IRRs may be set by the sponsor, and each “hurdle,” or return threshold, must be met before the sponsor can take an increasingly larger portion of the profits. For example, a sponsor offers an 8% IRR and then an 80%/20% split to a 16% IRR, then a 70%/30% split to an 18% IRR and a 60%/40% split thereafter. The sponsor is offering that all investors will receive the available cash flow (pro rata according to each investor’s initial contribution) until an 8% IRR, without any outsized profit given to the sponsor. Once an 8% IRR is reached, potential distributions will go through a second hurdle where investors receive 80% of the cash flow until they reach a 16% IRR. Once the investors achieve a 16% IRR, the investor will then receive 70% of the potential cash flow until an 18% IRR is reached. If the deal performs above an 18% IRR, investors would receive 60% of the proceeds thereafter. The purpose of this structure is to incentivize the sponsor to outperform.

To determine the IRR at each stage, Microsoft Excel takes aggregate capital invested and compounds it at the annual rate to calculate the amount of cash flow and return of capital to at least achieve the targeted IRR.

2. Preferred Return Promote Methodology

The second methodology for determining waterfalls is the preferred return promote methodology, which can be broken up into two main sub-categories; the first prioritizes a return of capital and the second allows profit from cash flow.

Return of Capital

In the first type of preferred return waterfall model, the sponsor prioritizes returning the investor’s capital investment before the sponsor receives its promote. The preferred return promote offers investors a preferred return (which may or may not compound), then a return of capital and only then will the sponsor receive its promote, generally at the time of sale. The preferred return can either be calculated off the original amount invested or the balance of invested capital (aka based on a declining principal amount).

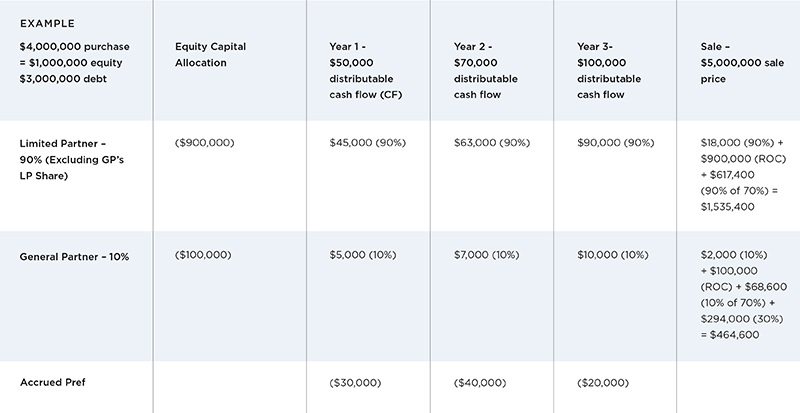

Below is an example which shows:

An 8% preferred return calculated on capital invested and noncompounding;

Then, a return of capital;

Thereafter, a 70/30 split:

Because the investor’s return of capital occurs before the sponsor’s promote, this is a more favorable structure to investors than a cash flow promote.

In the example above, the 8% preferred return accrues (but does not compound), which means if it is not paid in full in any given year, it carries forward and is paid in future years. At sale or refinance, the proceeds first pay off the senior lender’s debt, then any accrued and unpaid 8% preferred return ($20,000), then return the investor’s capital investment ($900k to LPs and $100k to GP), and then 70% to investors (90% of 70%, or $617,400, to LPs and 10% of 70%, or $69k, to GPs), and the 30% promote ($294k) just to the GP. Investors should always work with their sponsor and CPA to determine how and when to report the return of capital on their taxes for a given investment opportunity.

Promote off of Cash Flow

In the second type of preferred return waterfall model, the sponsor prioritizes reaching the promote by taking a promoted interest from annual cash flow before the investors receive their full return of capital. In this waterfall structure, investors first get a preferred return, then there is a split of any excess cash flows – some % to the sponsor and some % to investors. Initial capital is typically returned at the time of sale or refinance.

Below is an example which shows:

An 8% preferred return calculated on capital invested and non-compounding;

Thereafter, a 70/30 split (with the caveat that upon a capital event, a return of capital comes before any promote):

Because the sponsor’s promote occurs before the investor’s return of capital, this is a more favorable structure to sponsors, but it may be more appropriate for transactions that have a long hold period. In the example above, the 8% preferred return on the initial capital invested accrues, which means if it is not paid in full in any given year it carries forward and is paid in future years. In year one, only $70,000 is distributed, so $10,000 is carried forward to year two. In year two, the $80,000 preferred return plus the $10,000 carried forward preferred return are combined and paid out pro rata, but because there is an extra $10,000 above the 8% return, the investor gets 90% of 70% and the sponsor gets 10% of 70% (as an investor) and 30% promote. At sale or refinance, the purchase price proceeds first pay off the senior lender’s debt, then any accrued and unpaid 8% preferred return (none in the example), then returns the investor’s capital investment ($900k to LPs and $100k to GP), and then 70% to investors (90% of 70%, or $1.53M, to LPs and 10% of 70%, or $70k, to GPs), and the 30% ($300k) just to the GP.

3. Simple Split

The final method of determining a waterfall model is the simple split, which may not have any preferred return to the investors. An example might be 50% of all cash flow and profit is paid to investors and 50% of all cash flow is paid to the GP/sponsor. This is common in transactions where there may not be a high level of sophistication or lots of expenses, and the intent is to keep distributions very simple. An investor should ask in such instances if the sponsor is putting any capital into the transaction, whether the sponsor is contributing “sweat equity” (work as opposed to capital), and, if the sponsor is contributing capital, whether the sponsor is to receive its pro rata share of the investor portion of the distribution.

In Summary

Waterfalls are often not easy to model or to describe in operating agreements, so they should be done carefully and reviewed by professionals with years of experience. The success of an investment from an investor’s return perspective may depend upon well-defined distributions that are appropriately allocated to the proper parties during the hold period of the investment.

1. Not all Crowdfunding companies aggregate investors into an investment vehicle. A single purpose entity is one that has one business purpose, in this case to make an investment into the vehicle acquiring the investment property.

-

ARTICLE

COMMERCIAL REAL ESTATE

Lifecycle of a Commercial Real Estate Deal

Ram Realty Trust sources most of its transactions from inbound leads, meaning that real estate companies are actively pursuing the capital that we offer, and we sift through all of the requests to select those that match our investment criteria.

Read More...

Originations and Underwriting

Before a deal finds its way onto the Ram Realty Trust platform, it must pass through a series of steps to ensure that the transaction, the operator, and the real estate all meet Ram Realty Trust’s stringent criteria. Ram Realty Trust sources most of its transactions from inbound leads, meaning that real estate companies are actively pursuing the capital that we offer, and we sift through all of the requests to select those that match our investment criteria. In some cases, deals may be sourced through outbound business development, however given the number of requests we receive on an annual basis, we are usually unable to touch every request. Of all the deals we scrutinize, only a small minority actually meet all the criteria of our rigorous underwriting process.

At this stage, a deal may be rejected for reasons such as: We do not invest in that asset type or business plan (e.g. single tenant, development), the real estate company is not established enough to provide capital to or the real estate is located in a market that Ram Realty Trust is not interested in transacting in. If a deal makes it past the initial screening process, it must then pass through Ram Realty Trust’s investment committee approval process. At this stage, Ram Realty Trust does a deep dive into the due diligence and underwriting of the deal. Ram Realty Trust visits the property, does a zero-based underwriting (to generate a non-biased analysis) and negotiate the structure of the deal. If the deal holds up in investment committee, the deal may make its way onto the site to begin fundraising.

Closing an Investment

Once all the funds have been raised, the deal moves to the closing stage. At this point, most of the deal terms have been finalized and all that remains is to reconcile the outstanding debits and credits with the lender, the title company and any other parties that are to be paid at closing. The closing process rarely goes smoothly, with numbers usually being shifted around up until the final moments, so the Ram Realty Trust team is deeply involved every step of the way to ensure that everything is double-checked before our funds are released.

Asset Management

Once the deal has closed, the real estate company commences execution of the business plan, which as with closing, rarely goes exactly according to plan. Asset management refers to the ongoing monitoring and management of the investment throughout the hold period. Sponsor reports are provided quarterly and are investors’ best resource to track the performance of their investments. As such, ongoing review of these reports is key to successful asset management. This includes ensuring the reports are complete, analyzing the financials and balance sheet, comparing the property’s financials to proforma, and more. Oftentimes, we find ourselves asking the sponsors follow-up questions that come up as a result of this review. Ram Realty Trust’s Asset Management team translates the quarterly reports into an easy-to-review summary and provides them to investors along with the Sponsor reports.

One of the benefits of aggregating investors into Ram Realty Trust controlled Single Purpose Entities is that we may make up an amount of the deal equity, and as such, have control rights over certain aspects of the deal. In some cases where the business plan has gone too far off track, Ram Realty Trust’s Asset Management team will step in and enact changes or negotiate favorable outcomes on our investors’ behalf. Examples of this include calling for a change in property management, pushing to sell the property or negotiating a buyout of our investors’ interests.

Disposition

When the time comes to sell the property, either due to completion of the business plan or to take advantage of favorable market conditions, disposition of the asset is where the value created is realized. Most of the transactions on Ram Realty Trust’s platform are ‘’value-add’’ investments, meaning that much of the gain on the investment comes from the eventual sale as opposed to the distributions made during the hold period. Some of the transactions on Ram Realty Trust’s platform have an investment horizon of 3-5 years, however the actual hold period may vary based on market conditions, business plan execution, or other macro-economic conditions. Oftentimes, the property may be held longer than the original business plan in order to maximize investor value.

The Ram Realty Trust Difference

Ram Realty Trust views investor protection, due diligence, and strict underwriting discipline as the core strengths of our investing platform. Our strategy is quality over quantity, and instead of just being a middle man passing deals along, we want to be a partner to our investors, helping them to better navigate the complex decision making that comes with real estate investing.

-

ARTICLE

INVESTING

10 Important Things to Know About Investing in Opportunity Zones

Opportunity Zones are surging in popularity but they are also complex. Learn the 10 things you need to know before investing.

Read More...

Opportunity Zones were created to spur job growth and economic development in low-income communities by offering investors an incentive to place capital into underdeveloped markets. While interest has been increasing over the past year, there are 10 important things to know about Opportunity Zones before deciding to invest.

1. Over 8,700 Opportunity Zones to Choose From

There are over 8,760 Qualified Opportunity Zones in all 50 States, the District of Columbia, and five U.S. territories. The 2017 Tax Cuts and Jobs Act (TCJA) created the Opportunity Zone Program, which is intended to stimulate economic development and job creation with long-term investments in low-income neighborhoods.1

2. Three Benefits of Opportunity Zone Investing

Any business or individual with capital gains from the sale of an investment asset can receive tax benefits for investing unrealized capital gains in Opportunity Zones:2

Payment of the tax on previously earned capital gains that are reinvested in an Opportunity Zone is deferred until the end of 2026 (or when the asset is sold)

Basis of the original investment is increased by 10% if the Opportunity Zone investment is held for at least five years

Additional capital gains produced from the Opportunity Zone investment are permanently excluded from capital gains tax, provided the investment is held for at least 10 years

3. Key Opportunity Zone Terms to Understand

THERE ARE THREE KEY TERMS TO UNDERSTAND ABOUT OPPORTUNITY ZONES:

QOZ: Qualified Opportunity Zone is a low-income community census traded designated by each state or territory and approved by the federal government

QOF: Qualified Opportunity Fund is a corporation or partnership formed for the express purpose of investing equity into a Qualified Opportunity Zone property

QOZP: Qualified Opportunity Zone Property can be real estate or business property, corporate stock, or a partnership interest in an entity the does business primarily in a QOZ

4. Pay Zero Dollars in Capital Gains Tax

For long-term investors, the real bonus in QOZ investing comes after 10 years.3 That’s because after a 10-year holding period, the investment basis is stepped-up to fair market value, which means any appreciation can be sold tax-free.

As an example, consider a $500,000 investment that appreciates in value and is sold after being held for at least 10 years. If the property value increased to $750,000 the entire amount would be a tax-free gain. Of course, as with any other investment, appreciation is never guaranteed due to the specific financial performance of the investment and normal economic cycles.

5. Anyone With a Capital Gain Can Invest in OZs

While real estate investors have long benefited from conducting 1031 exchanges, capital gains from other investments were subject to tax. All of that changed when the TCJA of 2018 was signed into law.

Now, investors with gains from other assets such as stocks and bonds, precious metals, a business, and real estate can choose to invest those capital gains in an Opportunity Zone in order to defer or eliminate some of the gain for tax purposes.4

6. Opportunity Zone Investing Can Be Like a Turbocharged 1031

For real estate investors, investing in an Opportunity Zone has been described by some investors as a 1031 exchange on steroids.5 There are two reasons for this:

Unlike a 1031 exchange which requires reinvestment of the sales proceeds, only the capital gains portion from the investment sale needs to be reinvested in a QOF to receive preferential tax treatment

Real estate investors have a full 180 days to identify and close on the replacement QOZ investment, versus the more limited 45-day identification period of a 1031 tax deferred exchange

7. OZs May Simplify Investment Portfolio Diversification

In August of this year, The Council of Economic Advisers (CEA) published The Impact of Opportunity Zones: An Initial Assessment.6 The CEA report compares the advantages of OZs to other Federal economic development programs, and documents the characteristics of the over 8,700 low-income communities designated as Opportunity Zones.

For investors, one of the key benefits of placing capital gains in an OZ may be the ability to easily diversify an investment portfolio. That’s because a large percentage of Qualified Opportunity Funds used to invest in OZs have pooled investments across other industries in the OZ, such as health care, technology, and construction in addition to real estate:

45% of QOFs are pooled investment funds across various industries

22% focus on multiple real estate asset classes

18% invest in commercial real estate

9% invest in other assets such as businesses or infrastructure

6% invest in residential real estate

8. Asset Values Increase with Opportunity Zone Designation

The CEA report also learned that census tracts receiving an OZ designation saw a 29% relative increase in equity investment, leading to larger appreciation in housing prices and improved local amenities for renters.

Housing value increases in Opportunity Zones have led to an estimated $11 billion in additional wealth for the nearly half of OZ residents who own their home. Commercial real estate investors have also benefited from Opportunity Zone investments as well:

Growth in development site acquisitions increased by 50% year-over-year inside designated OZs, greatly exceeding growth in the rest of the U.S.

Prices of redevelopment properties in OZs increased by 14%

Prices of vacant development sites in OZs increased by 20%

9. Post-COVID-19 Recovery Boosted by Opportunity Zones

The Impact of Opportunity Zones: An Initial Assessment report from the CEA notes that the available evidence shows that Qualified Opportunity Funds are well positioned to invest in communities in 2020.

In the first quarter of this year, the pandemic triggered a massive selloff in the stock market that very likely generated significant capital gains for investors exiting a long-term bull market. While numerous State-mandated restrictions to slow the spread of COVID-19 have slowed investment everywhere, the CEA believes that capital raised by QOFs grew by about 30% during the first four months of 2020.

The performance of Opportunity Zones before COVID-19 suggests that the OZ model can continue to spur economic recovery post-COVID-19 as well. Capital is mobilized with limited control from the Federal Government, allowing investors to work with local stakeholders to help low-income communities grow and prosper.

10. Not All OZ Investments Offer Equal Opportunity

As with any other type of investment, not all Opportunity Zones provide the same amount of opportunity. Although the opportunity to save on taxes can be very attractive, investors should always be aware that a risky investment could be cloaked inside an OZ investment.7

For example, land and buildings within an Opportunity Zone may have already appreciated to such a degree that there is less potential profit remaining for incoming investors. Also, while some QOFs are diversified across various industries, high costs may offset much of the anticipated tax benefits.

For these reasons and more, potential investments within an OZ should be analyzed based on their own merits and potential performance, and not solely for the tax benefits provided.

Ram Realty Trust, LLC. and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction. See offering documents for additional details, disclosures, and disclaimers.

References

1. https://www.eda.gov/opportunity-zones

2. https://www.taxpolicycenter.org/briefing-book/what-are-opportunity-zones-and-how-do-they-work

3. https://www.cpexecutive.com/post/5-things-to-know-about-opportunity-zone-deadlines/

4. https://www.bizjournals.com/nashville/news/2019/06/17/5-things-to-know-about-opportunity-zones.html